Turning ambition into action: A guide to regulatory shifts in transition planning

In the face of geopolitical, economic, and climate uncertainty, good planning is essential. That is why even as the conversation on sustainability evolves, pressure is rising for financial institutions and corporates to develop credible transition plans. Once seen as voluntary exercises in long-term ambition, these plans are now core components of regulatory compliance, investor confidence, and business strategy.

Below, we help you understand the latest regulatory frameworks as well as how your organisation can apply them to design transition plans that are both compliant and strategically effective.

What Is a Transition Plan?

A transition plan sets out how an organisation will adapt its operations, business model, and investment decisions to align with climate goals and a changing world. The UK’s Transition Plan Taskforce (TPT) was created at COP 26 in Glasgow to provide guidance on the development and creation of effective transition Plans. The TPT stated that transition plan credibility depends on three principles:

- Ambition – clear targets aligned with climate science.

- Action – concrete near-term steps to achieve those targets.

- Accountability – governance and reporting to ensure delivery.

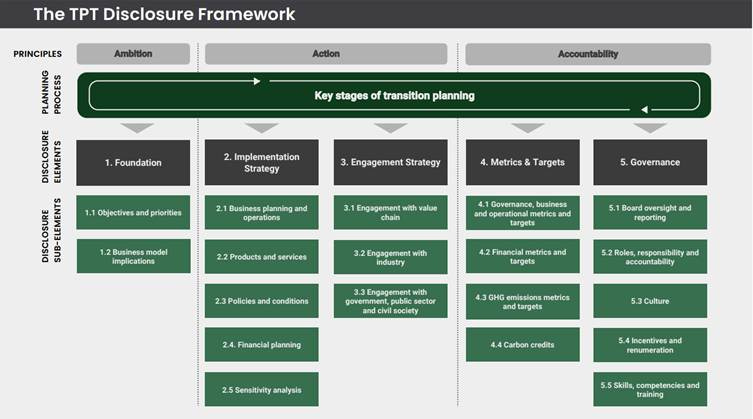

These principles underpin the TPT framework, which has since been adopted by the IFRS Foundation’s International Sustainability Standards Board (ISSB). In June 2025, the ISSB published official guidance under IFRS S2 that builds directly on the TPT materials. Materials from TPT and ISSB provide five interlocking pillars for effective transition plans.

Firms should consider the five pillars below as they develop their transition plans.

1. Foundations - Describes how the organisation positions its strategy within the transition to a low‑carbon economy, sets its ambition, and establishes credibility with reference to science-based targets and broader societal goals.

2. Implementation Strategy - Outlines specific actions, policies, and levers management will deploy to deliver on stated ambition, such as capital allocation, R&D, M&A decisions, and operational changes.

3. Engagement Strategy -Addresses how the organisation interacts with stakeholders, including clients, suppliers, workers, regulators, and communities, ensuring that the transition is achieved in a just and inclusive way.

4. Governance -Clarifies accountability structures, board-level oversight, remuneration links, and decision-making processes that embed transition delivery into corporate governance.

5. Metrics & Targets -Sets out key indicators, milestones, and financial and non-financial KPIs that allow progress to be tracked over time.

The Rise of Regulatory Adoption

Over the past few years, transition planning has moved from a new, “nice to have” in many jurisdictions to an emerging regulatory expectation. In addition, the International Transition Plan Network (ITPN) was created to help policymakers and institutions develop transition plans and set requirements around them. Here is a look at some of those developing mandates across jurisdictions. It is not exhaustive.

European Union (EU)

Under CSRD/ESRS, climate standard ESRS E1 explicitly includes a disclosure requirement for a “Transition plan for climate change mitigation,” further supported by EFRAG’s 2024 implementation guidance.

United Kingdom (UK)

The UK’s TPT produced a comprehensive disclosure framework that is now referenced by the ISSB as good practice for meeting IFRS S2 transition-plan disclosures.

Canada

OSFI updated Guideline B-15 on climate risk management in 2025 and signalled further updates to disclosure expectations (including transition plans and scenario analysis) with implementation dates to be determined.

Singapore

Authorities are adopting ISSB-aligned climate disclosures, with key requirements beginning from FY2025 for listed companies; SGX subsequently announced extended timelines for several elements to support implementation.

Hong Kong

Enhanced HKEX climate disclosure requirements took effect on 1 January 2025, and Hong Kong introduced ISSB-aligned Sustainability Disclosure Standards (HKFRS SDS) for voluntary adoption from August 2025, with an expectation of mandatory application by 2028.

Preparing for the Path Forward

For companies, transition plans need to evolve from static reporting documents into dynamic strategies that drive governance, operations and client engagement.

Applying the transition planning framework effectively means:

- Grounding plans in strong foundations with credible long-term ambition

- Translating ambition into delivery through a realistic implementation strategy

- Embedding a clear engagement strategy to secure stakeholder buy-in and avoid social pushback

- Strengthening governance structures to ensure accountability at the board level

- Tracking progress transparently with robust metrics and targets

In a world of intensifying scrutiny and rising transition risks, firms that align ambition with action and transparently report their progress will be better placed to manage risk, maintain stakeholder confidence and lead in a rapidly changing economy.

Enjoyed this analysis? D. A. Carlin & Co helps clients navigate these turbulent times through strategic briefings, practical capacity-building workshops, and regulatory support. Book a call with us today through our "Speak with us" form and find out how we can give you and your team the future-ready skills and strategies you need.